By Blake Davis, M&A Advisor, DMA (Divest Merge Acquire)

Buried in the FY27 Budget fact sheets is a worked example that every business owner contemplating a sale should pay attention to. It involves how capital gains are split between the old and new tax regimes, and the method Treasury has signaled could shift hundreds of thousands of dollars, sometimes more, into a higher-tax bucket.

Most of the commentary around the Budget has focused on the headline changes. From 1 July 2027, capital gains for individuals, partnerships and trusts will move from the current 50% CGT discount to a new framework: indexation of the cost base plus a 30% minimum tax on real gains. That shift alone is significant. But the detail that matters most for mid-market business sellers is not the rate change itself. It is how gains that straddle the 1 July 2027 boundary will be apportioned between the old and new regimes.

The Worked Example That Tells the Story

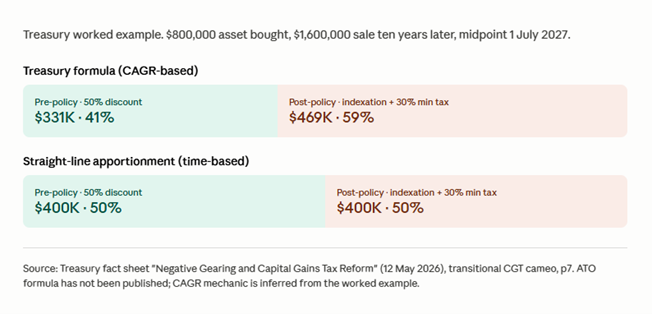

Treasury’s fact sheet includes a specific scenario. An asset purchased for $800,000 is sold ten years later for $1.6 million, with the midpoint of ownership falling on 1 July 2027. The total gain is $800,000.

If Treasury used a simple straight-line apportionment, the gain would be split evenly: $400,000 to the pre-policy period (taxed under the old 50% discount) and $400,000 to the post-policy period (taxed under the new, less favourable regime).

That is not what Treasury did. Instead, the example values the asset at $1.13 million on 1 July 2027, derived by compounding the original cost base at the asset’s overall annual growth rate (CAGR). The effect is that roughly $330,000 of the gain is allocated to the old regime and $470,000 to the new one. Close to 60% of the total gain ends up in the higher-tax bucket.

For an asset that has been compounding well, which is exactly the profile of a successful business, the CAGR method systematically allocates a larger share of the gain to the post-policy period. This is not a rounding difference. It is a structural feature of compound growth, and it works against the seller.

Scale This to a Mid-Market Business Sale

The Treasury example uses a relatively modest asset. Scale the same maths to a business with an enterprise value of $10 million or $20 million and the apportionment difference between straight-line and CAGR runs into the millions. The gain allocated to the new regime, and therefore subject to the 30% minimum tax on real gains rather than the 50% discount, becomes materially larger.

For a business owner who has built value steadily over 15 or 20 years, much of that compounding growth will be attributed to the post-2027 period under this method. That is a meaningful hit to after-tax sale proceeds.

What We Do Not Yet Know

The precise ATO formula has not been published. Treasury’s worked example is the strongest signal available, but it is still a fact sheet illustration, not legislated methodology. There are important questions that remain open. The ATO has indicated that a valuation can be obtained to crystallise the cost base at the start of the new regime. However, the specific requirements of the valuation are not yet detailed. In relation to the ATO formula – wow will the formula treat businesses where growth has been uneven or back-ended? What happens where the gain relates to goodwill that has been built up over decades?

It will also be worth watching whether this concept survives through to the final legislation in its current form.

The Practical Implication for Business Owners

If CAGR-based apportionment is confirmed, business owners contemplating a sale beyond mid-2027 face a clear decision: obtain a contemporaneous valuation at or around 30 June 2027, or accept whatever the formula produces.

A formal valuation at the transition date would provide an independently supportable figure for the pre-policy gain, potentially delivering a more favourable split than a backward-looking compound growth calculation. The cost of obtaining that valuation would be modest relative to the tax difference at stake.

For owners who are already in a sale process, the timing implications are obvious. A transaction that completes before 1 July 2027 avoids the new regime entirely. For those on a longer timeline, the apportionment question becomes a planning consideration that should be addressed in the near term and not left until a transaction takes place.

Where This Fits in Sale Planning

At DMA, we work closely with our clients’ tax advisors to ensure that transaction structuring accounts for the tax environment at the time of sale. The FY27 Budget changes add a new dimension to that planning. For business owners who have not yet engaged their accountant or tax advisor on this specific issue, it is worth doing so promptly. The interaction between deal structure (asset sale vs share sale, earnout timing, deferred consideration) and the new CGT regime will require careful analysis specific to each owner’s circumstances.

This is not a reason to panic, but it is a reason to plan. The businesses that navigate regulatory change well are those that see it early and build it into their strategy, not those that discover it during a transaction.

This article is provided for general information purposes only and does not constitute legal, financial, or tax advice. Business owners should seek professional advice in relation to their specific circumstances.

Link to the Treasury worked example: budget.gov.au/content/factsheets/download/tax-explainers-negative-gearing-capital-gains-tax.pdf

Blake Davis is an M&A Advisor at DMA (Divest Merge Acquire),. For a confidential discussion about your business or transaction, contact DMA at blake.davis@divestma.com